Original Copied from http://stormthunder.com/#ixzz2mGlGZ9fA

Under Creative Commons License: Attribution Non-Commercial No Derivatives

Tax Exemption

Tax Exemption Through Use of Lawful Money to End the Fed

The truth about the income tax, the national debt, the Federal Reserve, and what you can do about it.

Send this page to everyone you know. Post it on your Facebook, send it to your email address book, get the word out that the days of slavery are over.

Notes

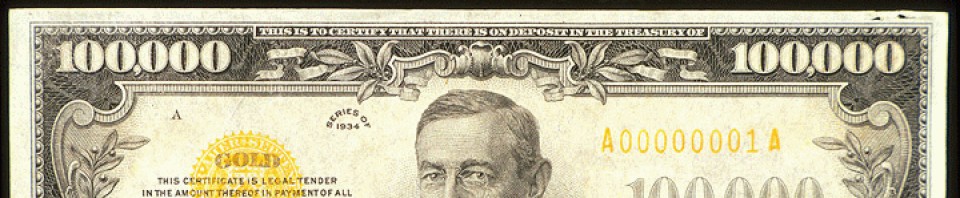

Top: Federal Reserve Note. Bottom: United States Note

Besides the “Federal Reserve Note” on the scroll at the top of the note, the fed note has a green seal and serial numbers and the US note has red.

Use the green money, the debt grows and you own nothing. Use the red money, the debt goes down, you are tax exempt, and you own what you buy. Simple as that.

The following article explains the legalities in detail, along with the remedy. THIS IS NOT THEORY, THIS IS FACT. IGNORE THIS AND YOU DESERVE WHAT’S COMING:

Public Money vs. Private Credit

July 4, 1861 Abraham Lincoln re-convenes congress under an ‘extraordinary occasion’ that is technically still in-place today [Lincoln’s order convening Congress was by proclamation set forth 15 April 1861]. It had adjourned sine die since March 28 1861 [by March 28, the southern congressmen had walked out of session. That, combined with uncertainty as to Lincoln’s military intentions, led the remaining members of the 37th Congress to agree to adjourn without setting a day to reconvene — sine die means without day]. The congress today is still a [Lincoln convened, executive] de-facto congress. [To my knowledge, congress still adjourns sine-die, informing members of the re-convention date during the recess]

Twenty eight days prior to congress adjourning sine die, we find that the territory of Colorado was formed and would have taken 30 days to form properly. President Buchannan was actually lining up Colorado with the gold claims found in Aurora and Central City to be the war chest for prosecuting the war between the states [erroneously referred to by many as a civil war — which it was not] from the union side. Colorado was basically a union state.

President Lincoln got the election, so he moved into President Buchanan’s plans. The first territorial governor, governor Gilpen, issued notes. These are the predecessors to the United States notes called green-backs. If we take a look at the treasury, their website, we find this particular page regarding legal tender

http://www.ustreas.gov/education/faq/currency/legaltender.shtml

Legal tender status. Now pay particular notice to the bottom of the page:

United States notes serve no function that is not already adequately served by Federal Reserve notes. As a result, the Treasury Department stopped issuing United States notes, and none have been placed into circulation since January 21, 1971.

[Article published by Freedom League 1984:]

When Congress borrows money on the credit of the United States, bonds are thus legislated into existence and deposited as credit entries in Federal Reserve banks. United States bonds, bills and notes constitute money as affirmed by the Supreme Court (Legal Tender Cases, 110 US 421), and this money when deposited with the Fed becomes collateral from whence the Treasury may write checks against the credit thus created in its account (12 USC 391). For example: suppose Congress appropriates an expenditure of $1 billion.

To finance the appropriation, Congress creates the $1 billion worth of bonds out of thin air [actually, created upon a presumption — see David’s comment below] and deposits it with the privately owned Federal Reserve System. Upon receiving the bonds, the Fed credits $1 billion to the Treasury’s checking account, holding the deposited bonds as collateral. When the United States deposits its bonds with the Federal Reserve System, private credit is extended to the Treasury by the Fed.

Under its power to borrow money, Congress is authorized by the Constitution to contract debt, and whenever something is borrowed it must be returned. When Congress spends the contracted private credit, each use of credit is debt which must be returned to the lender or Fed.

Since Congress authorizes the expenditure of this private credit, the United States incurs the primary obligation to return the borrowed credit, creating a National Debt which results when credit is not returned. However, if anyone else accepts this private credit and uses it to purchase goods and services, the user voluntarily incurs the obligation requiring him to make a return of income whereby a portion of the income is collected by the IRS and delivered to the Federal Reserve banksters.

Actually the federal income tax imparts two separate obligations: the obligation to file a return and the obligation to abide by the Internal Revenue Code. The obligation to make a return of income for using private credit is recognized in law as an irrecusable obligation, which according the Bouvier’s Law Dictionary (1914 ed.), is “a term used to indicate a certain class of contractual obligations recognized by the law which are imposed upon a person without his consent and without regard to any act of his own”.

This is distinguished from a recusable obligation which, according to Bouvier, arises from a voluntary act by which one incurs the obligation imposed by the operation of law. The voluntary use of private credit is the condition precedent which imposes the irrecusable obligation to file a tax return. If private credit is not used or rejected, then the operation of law which imposes the irrecusable obligation lies dormant and cannot apply.

In Brushaber v. Union Pacific RR Co., 240 US 1 (1916) the Supreme Court affirmed that the federal income tax is in the class of indirect taxes, which include duties and excises. The personal income tax arises from a duty — i.e., charge or fee — which is voluntarily incurred and subject to the rule of uniformity. A charge is a duty or obligation, binding upon him who enters into it, which may be removed or taken away by a discharge (performance) Bouvier, p 459.

Our federal personal income tax is not really a tax in the ordinary sense of the word but rather a burden or obligation which the taxpayer voluntarily assumes, and the burden of the tax falls upon those who voluntarily use private credit. Simply stated, the tax imposed is a charge or fee upon the use of private credit where the amount of private credit used measures the pecuniary obligation.

The personal income tax provision of the Internal Revenue Code is private law rather than public law. “A private law is one which is confined to particular individuals, associations, or corporations”: 50 Am.Jur.: 12 p 28. In the instant case the revenue code pertains to taxpayers. A private law can be enforced by a court of competent jurisdiction when statutes for its enforcement are enacted: 20 Am.Jur.: 33. pg. 58, 59.

The distinction between public and private acts is not always sharply defined when published statutes are printed in their final form: Case v. Kelly, 133 US 21 (1890). Statutes creating corporations are private acts: 20 Am.Jur. 35, p 60. In this connection, the Federal Reserve Act is private law. Federal Reserve banks derive their existence and corporate power from the Federal Reserve Act: Armano v. Federal Reserve Bank, 468 F.Supp. 674 (1979).

A private act may be published as a public law when the general public is afforded the opportunity of participating in the operation of the private law. The Internal Revenue Code is an example of private law which does not exclude the voluntary participation of the general public. Had the Internal Revenue Code been written as substantive public law, the code would be repugnant to the Constitution, since no one could be compelled to file a return and thereby become a witness against himself.

Under the fifty titles listed on the preface page of the United States Code, the Internal Revenue Code (26 USC) is listed as having not been enacted as substantive public law, conceding that the Internal Revenue Code is private law. Bouvier declares that private law “relates to private matters which do not concern the public at large.” It is the voluntary use of private credit which imposes upon the user the quasi contractual or implied obligation to make a return of income. In Pollock v. Farmer’s Loan & Trust Co., 158 US 601 (1895), the Supreme Court had declared the income tax of 1894 to be repugnant to the Constitution, holding that taxation of rents, wages and salaries must conform to the rule of apportionment.

However, when this decision was rendered, there was no privately owned central bank, issuing private credit and currency, but rather public money in the form of legal tender notes and coins of the United States circulated. Public money is the lawful money of the United States which the Constitution authorizes Congress to issue, conferring a property right, whereas the private credit issued by the Fed is neither money nor property, permitting the user an equitable interest but denying allodial title. [In other words, you cannot really ‘buy’ anything with Federal Reserve Notes.]

Today, we have two competing monetary systems: The Federal Reserve System with its private credit and currency, and the public money system consisting of legal tender United States Notes and coins. One could use the public money system, paying all bills with coins and United States notes (if the notes can be obtained), or one could voluntarily use the private credit system and thereby incur the obligation to make a return of income. Under 26 USC 7609 the IRS has carte blanche authority to summon and investigate bank records for the purpose of determining tax liabilities or discovering unknown taxpayers: United States v. Berg, 636 F.2d 203 (1980).

If an investigation of bank records discloses an excess of $1000 in deposits in a single year, the IRS may accept this as prima facie evidence that the account holder uses private credit and is therefore a person obligated to make a return of income. Anyone who uses private credit — e.g. bank accounts, credit cards, mortgages, etc — voluntarily plugs himself into the system and obligates himself to file.

A Taxpayer is allowed to claim a $1000 personal deduction when filing his return. The average taxpayer in the course of a year uses United States coins in vending machines, parking meters, small change, etc, and this public money must be deducted when computing the charge for using private credit.

On June 5, 1933, the day of infamy arrived. Congress on that date enacted House Joint Resolution 192, which provided that the people [actually, HJR-192 applied only to corporate persons, not to people] convert or turn in their gold coins in exchange for Federal Reserve notes. Through the operation of law, HJR-192 took us off the gold standard and placed us on the dollar standard where the dollar could be manipulated by private interests for their self-serving benefit. By this single act the people and their wealth were delivered to the bankers. When gold coinage was thus pulled out of circulation, large denomination Federal Reserve notes were issued to fill the void. As a consequence the public money supply in circulation was greatly diminished, and the debt-laden private credit of the Fed gained supremacy.

This action made private individuals who had been previously exempt from federal income taxes now liable for them, since the general public began consuming and using large amounts of private credit. Notice all the case law prior to 1933 which affirms that income is a profit or gain which arises from a government granted privilege.

After 1933, however, the case law no longer emphatically declares that income is exclusively corporate profit, or that it arises from a privilege. So, what changed? Two years after HJR-192, Congress passed the Social Security Act, which the Supreme Court upheld as a valid act imposing a valid income tax: Charles C. Steward Mach. Co v. Davis, 301 US 548 (1937).

It is no accident that the United States is without a dollar unit coin. In recent years the Eisenhower dollar coin received widespread acceptance, but the Treasury minted them in limited number which encouraged hoarding. This same fate befell the Kennedy half-dollars, which circulated as silver sandwiched clads between 1965 and 1969, and were hoarded for their intrinsic value and not spent. Next came the Susan B. Anthony dollar, an awkward coin which was instantly rejected as planned.

The remaining unit is the privately issued Federal Reserve note unit dollar with no viable competitors. Back in 1935 the Fed had persuaded the Treasury to discontinue minting silver dollars because the public preferred them over dollar bills. That the public money system has become awkward, discouraging its use, is no accident. It was planned that way.

A major purpose behind the 16th amendment was to give Congress authority to enforce private law collections of revenue. Congress had the plenary power to collect income taxes arising from government granted privileges long before the 16th Amendment was ratified, and the amendment was unnecessary, except to give Congress the added power to enforce collections under private law, i.e. income from whatever source.

So, the Fed got its amendment and its private income tax, which is a banker’s dream but a nightmare for everyone else. Through the combined operation of the Fed and HJR-192, the United States pays exorbitant interest whenever it uses its own money deposited with the Fed, and the people pay outrageous income taxes for the privilege of living and working in their own country, robbed of their wealth and separated from their rights, laboring under a tax system written by a cabal of loan shark bankers and rubber stamped by a spineless Congress.

Congress has the power to abolish the Federal Reserve System and thus destroy the private credit system. However, the people have it within their power to strip the Fed of its powers, rescind private credit and get the bankers to pay off the National Debt should Congress fail to act.

The key to all this is 12 USC 411, which declares that Federal Reserve notes shall be redeemed in lawful money at any Federal Reserve Bank. Lawful money is defined as all the coins, notes, bills, bonds and securities of the United States. Julliard v. Greenman, 110 US 421, 448 (1884): whereas public money is the lawful money declared by Congress as a legal tender for debts (31 USC 5103), 521 F.2d 629 (1974).

Anyone can present Federal Reserve notes to any Federal Reserve Bank and demand redemption in public money — i.e. legal tender United States notes and coins. A Federal Reserve note is a fixed obligation or evidence of indebtedness which pledges redemption (12 USC 411) in public money to the note holder.

The Fed maintain a ready supply of United States notes in hundred dollar denominations for redemption purposes should it be required, and coins are available to satisfy claims for smaller amounts. However, should the general public decide to redeem large amounts of private credit for public money, a financial melt-down within the Fed would quickly occur.

The process works like this: Suppose $1000 in Federal Reserve notes are presented for redemption in public money. To raise $1000 in public money the Fed must surrender US Bonds in that amount to the Treasury in exchange for the public money demanded (assuming that the Fed had no public money on hand). In so doing, $1000 of the National Debt would be paid off by the Fed and thus canceled.

Can you imagine the result if large amounts of Federal Reserve notes were redeemed on a regular ongoing basis? Private credit would be withdrawn from circulation and replaced with public money, and with each turning of the screw the Fed would be obliged to pay off more of the National Debt. Should the Fed refuse to redeem its notes in public money, then the fiction that private credit is used voluntarily would become unsustainable.

If the use of private credit becomes compulsory, then the obligation to make a return of income is voided. If the Fed is under no obligation to redeem its notes, then no one has an obligation to make a return of income. It is that simple! Federal Reserve notes are not money and cannot be tendered when money is demanded: 105 So. 305 (1925).

Moreover, the Ninth Circuit rejected the argument that a $50 Federal Reserve note be redeemed in gold or silver coin after specie coinage had been rescinded but upheld the right of the note holder to redeem his note in current public money (31 USC 392 rev., 5103): 524 F.2d 629 (1974), 12 USC 411.

It would be advantageous to close out all bank accounts, acquire a home safe, settle all debts in cash with public money and use US postal money orders for remittances. Whenever a check is received, present it to the bank of issue and demand cash in public money. This will place banks in a vulnerable position, forcing them to draw off their assets. Through their insatiable greed, bankers have over extended, making banks quite illiquid.

Should the people suddenly demand public money for their deposits and for checks received, many banks will collapse and be foreclosed by those demanding public money. Banks by their very nature are citadels of usury and sin, and the most patriotic service one could perform is to obligate bankers to redeem private credit.

When the first Federal Reserve note is presented to the Fed for redemption, the process of ousting the private credit system will commence and will not end until the Fed and banking system nurtured by it collapse. Coins comprise less than five percent of the currency, and current law limits the amount of United States notes in circulation to $300 million (31 USC 5115).

The private credit system is exceedingly over extended compared with the supply of public money, and a small minority working in concert can easily collapse the private credit system and oust the Fed by demanding redemption of private credit. If the Fed disappeared tomorrow, income taxes on wages and salaries would vanish with it. Moreover, the States are precluded from taxing United States notes: 4 Wheat. 316.

According to Bouvier, public money is the money which Congress can tax for public purposes mandated by the Constitution. Private credit when collected in revenue can fund programs and be spent for purposes not cognizable by the Constitution. We have in effect two competing governments: the United States Government and the Federal Government.

The first is the government of the people, whereas the Federal Government is founded upon private law and funded by private credit. What we really have is private government. Federal Agencies and activities funded by the private credit system include Social Security, bail out loans to bankers via the IMF, bail out loans to Chrysler, loans to students, FDIC, FBI, supporting the UN, foreign aid, funding undeclared wars, etc., all of which would be unsustainable if funded by taxes raised pursuant to the Constitution.

The personal income tax is not a true tax but rather an obligation or burden which is voluntarily assumed, since revenue is raised through voluntary contributions and can be spent for purposes unknown to the Constitution. Notice how the IRS declares in its publications that everyone is expected to contribute his fair share. True taxes must be spent for public purposes which the Constitution recognizes. Taxation for the purpose of giving or loaning money to private business enterprises and individuals is illegal: 15 Am.Rep. 39, Cooley, Prin. Const. Law, ch IV.

Revenue derived from the federal income tax goes into a private slush fund raised from voluntary contributions and Congress is not restricted by the Constitution when spending or disbursing the proceeds from this private fund. It is incorrect to say that the personal federal income tax is unconstitutional, since the tax code is private law and resides outside the Constitution.

The Internal Revenue Code is non-constitutional because it enforces an obligation which is voluntarily incurred through an act of the individual who binds himself. Fighting the Internal Revenue Code on constitutional grounds is wasted energy. The way to bring it all down is to attack the Federal Reserve System and its banking cohorts by demanding that private credit be redeemed, or by convincing Congress to abolish the Fed.

Never forget that private credit [central bank credit] is funding the destruction of our country.

[Reprinted from ‘Freedom League’, Sept/Oct 1984]

By demanding non-negotiable Federal Reserve Notes at the time of cashing any paycheck, you’re avoiding the taxable event:

Redeemed in lawful money Pursuant to 12 USC 411

:True Name: dba LEGAL NAME

You’re avoiding the activity — or the verb — of endorsement. [Actually, I believe it is a restrictive endorsement because it ‘restricts’ how the bank may negotiate the instrument.]

Negotiable instruments can be exchanged for other and presumably higher forms of currency. So a nonnegotiable Federal Reserve Note is a way of saying that you’re getting United States Notes instead. This is domestic emergency currency, instead of foreign emergency currency (Federal Reserve Notes). The problem with this non-endorsement as far as the bank is concerned, is that the bearer of the check is not pledging any credit; any private credit behind the check.

[The Story of Money — Federal Reserve Bank of New York]

The only bond behind the check is the presumed goods or services, and the full amount has to come out of the bank account of the drafter — whoever drafted the check. This means that the bank cannot do any fractional lending; for every $10 that’s put into the vault, they can’t lend out $90 more. And so this is what it means in the article by it diminishes the private credit. You’re actually redeeming the private credit from the Federal Reserve and putting it into public money form — non-negotiable Federal Reserve Notes. They still look like Federal Reserve Notes…

To summarize and paraphrase, the opening paragraphs of the article are a little misleading to say that the $1 billion in bond money is created out of thin air. It’s created, actually out of a suppositional wagering scheme or a tontine that everybody will be fooled into pledging themselves as national debt.

David Merrill

Statutory citations:

12 USC §391

Federal reserve banks as Government depositaries and fiscal agents.

The moneys held in the general fund of the Treasury, except the 5 per centum fund for the redemption of outstanding national-bank notes may, upon the direction of the Secretary of the Treasury, be deposited in Federal reserve banks, which banks, when required by the Secretary of the Treasury, shall act as fiscal agents of the United States; and the revenues of the Government or any part thereof may be deposited in such banks, and disbursements may be made by checks drawn against such deposits.

12 USC §411

Federal reserve notes, to be issued at the discretion of the Board of Governors of the Federal Reserve System for the purpose of making advances to Federal reserve banks through the Federal reserve agents as hereinafter set forth and for no other purpose, are authorized. The said notes shall be obligations of the United States and shall be receivable by all national and member banks and Federal reserve banks and for all taxes, customs, and other public dues. They shall be redeemed in lawful money on demand at the Treasury Department of the United States, in the city of Washington, District of Columbia, or at any Federal Reserve bank.

31 USC §5103

United States coins and currency (including Federal reserve notes and circulating notes of Federal reserve banks and national banks) are legal tender for all debts, public charges, taxes, and dues. Foreign gold or silver coins are not legal tender for debts. [Notice that there is no reference to ‘private’ obligations]

31 USC §5115

(a) The Secretary of the Treasury may issue United States currency notes. The notes—

(1) are payable to bearer; and

(2) shall be in a form and in denominations of at least one dollar that the Secretary prescribes.

(b) The amount of United States currency notes outstanding and in circulation—

(1) may not be more than $300,000,000; and

(2) may not be held or used for a reserve.

1 comment

this is very useful article for many users. thanks for putting across these details in this article.